מהפכת רווחי השיערוך של רשות המיסים הולכת להשפיע דרמטית על החברות בישראל: אלו שלושת השינויים שצריך לעשות בה, שלומי שוב וניר הלפרין (*)

רשות המיסים מנסה באופן תקדימי להגדיר בתקנות מה הם 'רווחי שיערוך' ובדרך משלימה, הלכה למעשה, הכרה מלאה בתקינת ה- IFRSברוח גישת העקיבה. מדובר בהרחבה דרמטית של ההסתכלות על רווחי שיערוך לצורכי מס, הרבה מעבר לרווחי שיערוך של נדל"ן להשקעה, כפי שנדונו בבתי המשפט וכפי שמקובל היום על פי רוב בפרקטיקה. על מנת שמהלך זה של רשות המיסים לא יהפוך ל"פיאסקו" הוא חייב לדעתנו לעבור 3 התאמות עיקריות: האחת, ניטרול רווחים רעיוניים שניתנים למימוש בנקל למזומן (כמו אלה שנובעים משיערוך ניירות ערך סחירים). השניה, אימוץ עקרון בסיסי לפיו בחירת מדיניות חשבונאית אפשרית ב- IFRS, לא תשנה את המצב המיסוי. וההתאמה השלישית

חברות כרטיסי האשראי צריכות לעבור ולדווח לפי ה- IFRS

ההתבדלות הבעייתית בכללי החשבונאות ״המיוחדים״ של הבנקים בישראל, שנמשכת כבר כמעט שני עשורים, רק הולכת ומתרחבת בעקבות ההתפתחויות הרגולטוריות של השנים האחרונות בכיוון תחרות. כך, חברות כרטיסי אשראי שכפופות לפיקוח על הבנקים, נדרשות להמשיך וליישם כללים חשבונאיים אלה גם אחרי שנפרדו מהבנקים וזה משתרשר גם לחברות הציבוריות שרוכשות את השליטה בהן. כלל ביטוח החזקות ביטוח כבר נאלצה להפסיק לחתום את דוחותיה המאוחדים ככאלה שערוכים לפי IFRS ובקרוב זה יגיע גם לדוחות המאוחדים של קבוצת דלק בעקבות רכישת ישראכרט

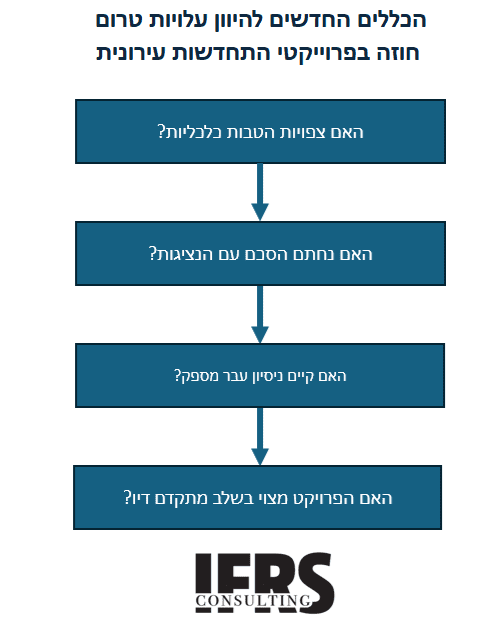

סוכריה חשבונאית לחברות ההתחדשות העירונית: הקדמת ההיוון של עלויות השגת חוזי פינוי בינוי

בעקבות עמדת סגל חדשה של רשות ניירות ערך שמסדירה את נושא הטיפול החשבונאי בעסקאות התחדשות עירונית, החברות העוסקות בתחום הפופולארי והלוהט בבורסה צפויות להקדים משמעותית את מועד ההיוון של עלויות טרום ביצוע כדוגמת עלויות משפטיות ובגין מחתימנים, תכנון, רישוי, היטלים ויועצים. מאחר ועד כה מועד ההיוון נקבע באופן שמרני מאד, המשמעות היא שיפור בתוצאות המדווחות של החברות בתחום שיהיה משמעותי במיוחד אצל רבות מהן שנמצאות כיום בצמיחה מואצת של פרויקטים חדשים. המהלך החשבונאי הנכון גם יוביל לקוהרנטיות עם תחומים אחרים, כמו חברות הפועלות בתחום האנרגיה הירוקה.

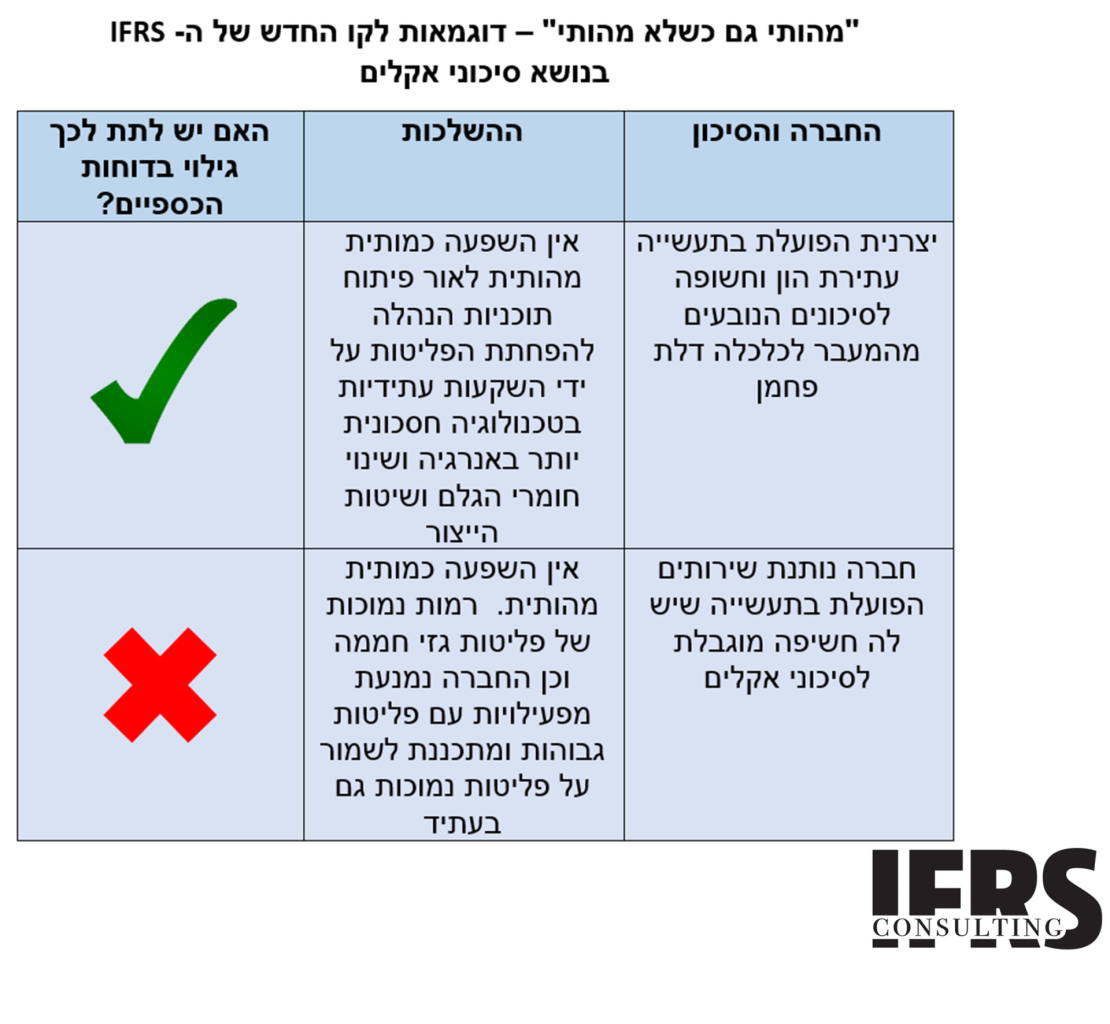

סיכוני האקלים מרחיבים את “גבולות הגזרה” של הדוחות הכספיים

ה- IFRS מחדד את הצורך בגילוי על סיכוני האקלים במסגרת הדוחות הכספיים עצמם וצפוי אף בקרוב לדרוש הפעלת שיקול דעת למתן גילוי גם במצבים שבהם אין דרישה ספציפית כזאת בתקנים החשבונאיים הקיימים. זאת לרבות במקרים בהם בעקבות תוכניות להתמודדות עם משבר האקלים הישות לא צופה השפעה מהותית על דוחותיה הכספיים! הרציונל בדרישה זו הוא שללא גילוי כזה המשתמשים השונים בדוחות עשויים לצפות שחלק מהנכסים (ועל כן ההון) עלולים להיפגע לאור התוכנית. היקף הגילוי ייגזר, בין היתר, מהתעשייה בה פועלת הישות כמו גם מהסביבה הרגולטורית בה היא פועלת. לקביעות החדשות עשויות להיות השלכות נגזרות גם על דרישות הגילוי בדוחות הכספיים לגבי

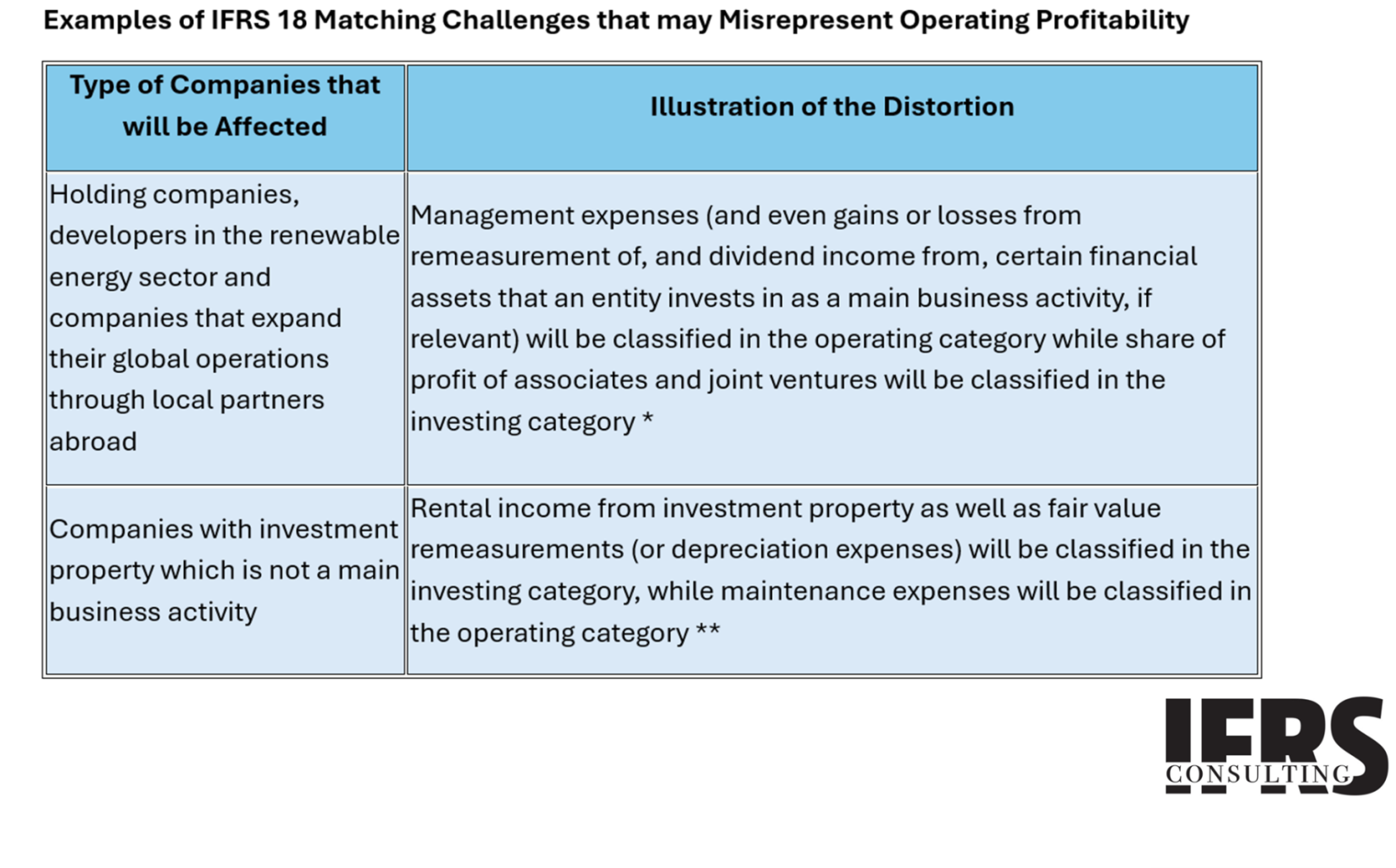

Inherent Distortion in IFRS 18: the Expected Impact on Operating Results of Companies Whose Main Business Activity Includes Investing in Associates and Joint Ventures Accounted for Using the Equity Method

array(40) { [0]=> int(9099) [1]=> int(9071) [2]=> int(9617) [3]=> int(9183) [4]=> int(9102) [5]=> int(9068) [6]=> int(10952) [7]=> int(35654) [8]=> int(35652) [9]=> int(35579) [10]=> int(12639) [11]=> int(12216) [12]=> int(12204) [13]=> int(12080) [14]=> int(9639) [15]=> int(9629) [16]=> int(9220) [17]=> int(9612) [18]=> int(9082) [19]=> int(11823) [20]=> int(11884) [21]=> int(13159) [22]=> int(11768) [23]=> int(12223) [24]=> int(12814) [25]=> int(12489) [26]=> int(11258) [27]=> int(9394) [28]=> int(22481) [29]=> int(12152) [30]=> int(12105) [31]=> int(9145) [32]=> int(12428) [33]=> int(12467) [34]=> int(10513) [35]=> int(12696) [36]=> int(12353) [37]=> int(33769) [38]=> int(12189) [39]=> int(13232) } FAILED: !is_front_page Companies that Invest in associates and joint ventures accounted for using the equity method as part of their main business activities may “fall between the cracks” under IFRS 18. This could be the case, for example, with holding companies, developers in the renewable energy sector and companies that expand their global operations through local partners […]

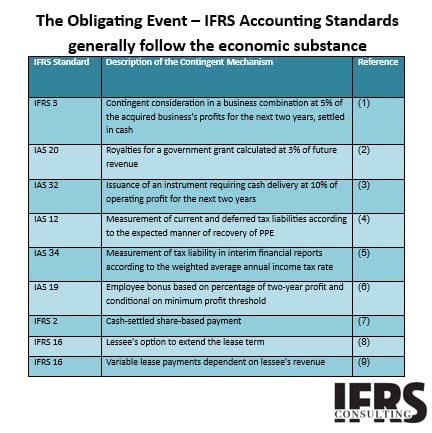

Off-Balance Sheet Financing: The Proposed Amendment to IAS 37 Demonstrates the Need to Recognise a Liability for the Acquisition of an Asset in Exchange for Performance-Based Contingent Consideration

Currently, IFRS does not provide an answer to the fundamental question of whether a financial liability arises from an obligation for contingent consideration that depends on the future performance of the acquirer in relation to the acquired asset, unless it involves a business combination. As a result, the practice in this area varies, and the acquisition of property, plant and equipment or an intangible asset in exchange for such contingent consideration may not appear at all in the statement of financial position.

The Missing Twist in the New Proposal for Amendments to IAS 28 on the Equity Method

The New ED Proposal deliberately avoids fundamental issues of what exactly is significant influence and whether the equity method is a measurement basis or a one-line consolidation. However, the key issue that should have been addressed is why a fair value model, which is more relevant to investors, is not adopted for associates. A preferable alternative solution is that a fair value measurement for investments in listed associates should be required, while it will be optional for non-listed associates.

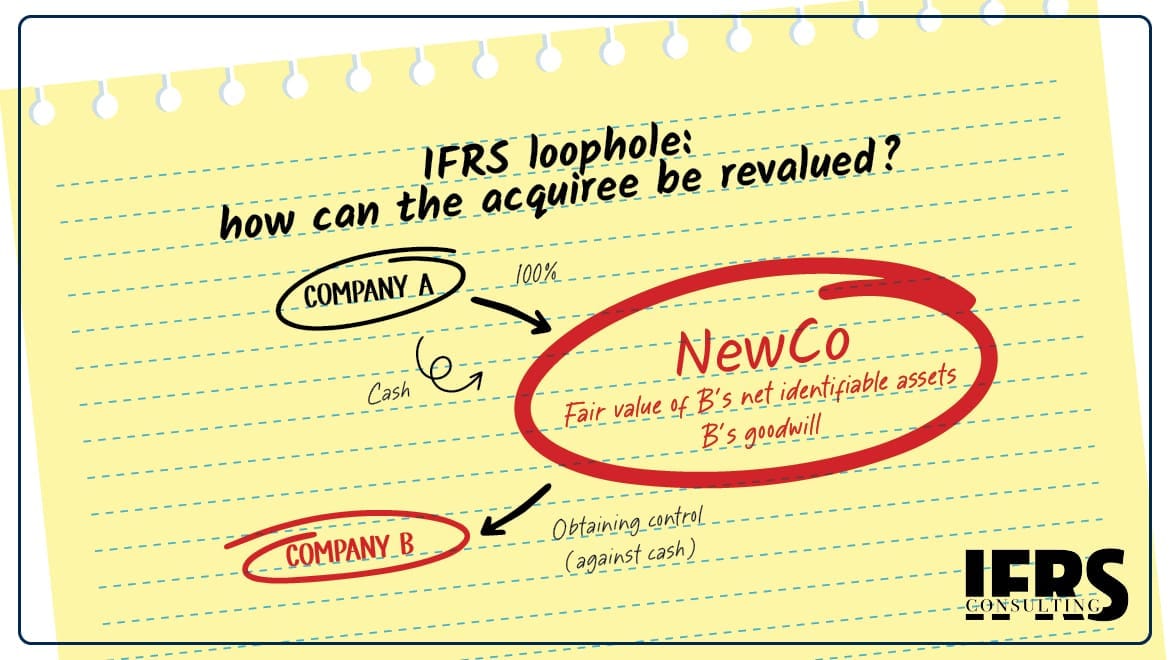

It is Time for the IFRS to Adopt Pushdown Accounting

Adopting the pushdown accounting model in IFRS will lead to a tremendous improvement in the relevance of financial statements without compromising their reliability. In line with a new extensive project taken by the IASB, and in view of the distortion resulting from the current cost accounting approach, this accounting model is an essential solution to the inadequate presentation of the economic value of intangible assets, which can constitute a significant portion of the value of many companies. Under this accounting model, upon a change in control a one-time revaluation of the acquired company's identifiable assets and liabilities and any goodwill

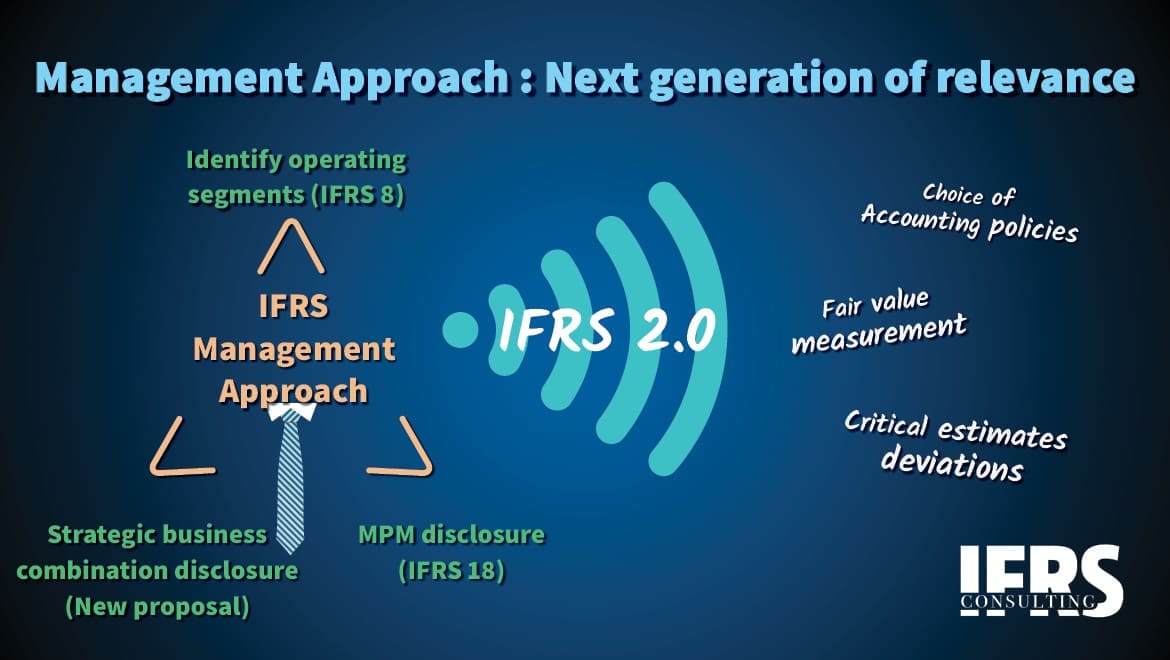

Unprecedented Disclosure Requirements in IFRS on Business Combinations: Where else should the Trend to adopt the Management Approach Go?

IFRS has taken a significant step forward with a proposal for disclosure requirements of management key objectives and related targets in strategic business combinations and the extent to which they are subsequently met. The background to this unprecedented disclosure stems from the concern that management may try to conceal failed business combinations. The proposal reflects a clear trend by the IASB to use the management approach to improve the relevance of financial statements. Shaking up traditional accounting and increasing auditor awareness of the business perspective through the management approach is also appropriate in several other accounting topics, such as the